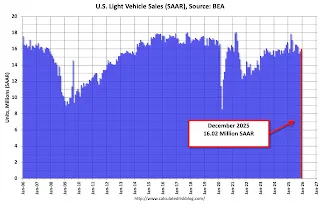

The latest data from the Bureau of Economic Analysis (BEA) highlights a noteworthy uptick in light vehicle sales for December, reaching 16 million units on a seasonally adjusted annual rate (SAAR). This marks a 1.9% increase from the previous month, although it reflects a decline of 4.9% compared to the same month last year.

Click on graph for larger image.

Click on graph for larger image.

Historically, consumer behavior is influenced by external factors such as tariffs and incentives. This is evident from earlier this year, when vehicle sales soared above 17 million SAAR in March and April as consumers aimed to "beat the tariffs." However, sales took a hit in May and June, followed by a surge in August and September as the expiration of EV credits spurred buying activity.

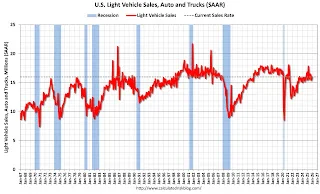

The second graph illustrates light vehicle sales from 1967 onwards. In a slightly positive twist, December's numbers exceeded analyst expectations, contributing to an overall growth of 2.4% in vehicle sales for 2025 relative to 2024.

The second graph illustrates light vehicle sales from 1967 onwards. In a slightly positive twist, December's numbers exceeded analyst expectations, contributing to an overall growth of 2.4% in vehicle sales for 2025 relative to 2024.

Analyzing December's Increase in Sales

The reported increase in vehicle sales to 16 million units on a seasonally adjusted annual rate is certainly noteworthy. While a growth of 1.9% from November suggests some restoration in buyer confidence, the comparison to December of last year reflects an ongoing struggle in the automotive sector, driven in part by changing consumer preferences and economic conditions. Indeed, the 4.9% decline when juxtaposed with one year prior raises eyebrows regarding the sustainability of any growth momentum.

Consumer patterns are often complex and apt to shift dramatically based on various socio-economic factors. Tariffs on imported vehicles and their parts have historically had an impact, often leading consumers to make hurried purchasing decisions to avoid potential price hikes. This year’s temporary surge before tariffs kicked in underscores how external policies can distort purchasing behavior, but such spikes don't usually translate into long-term stability.

The Role of Incentives and Manufacturer Strategies

Vehicle sales tend to spike when incentives are offered, like tax credits for electric vehicles (EVs), which not only drive sales volumes but also influence market trends over time. In the preceding months, the expiration of certain EV credits significantly impacted sales figures, as evidenced by the post-surge decline during the summer. August and September saw a notable uptick once consumers rushed to take advantage of the credits before their expiry. This cycle of incentivizing purchasing, though beneficial in the short term, can lead to volatility in sales figures across different quarters.

What remains pivotal is understanding manufacturers' responses to these incentives. Various automakers have tailored their inventory and pricing strategies to adapt to buyer behavior influenced by these external variables. If you're working in this space, you'll know that an emphasis on electric vehicles, coupled with competitive financing options and attractive trade-in offers, can help mitigate some of the downturns experienced when incentives fade.

Historical Context: Lessons from the Past

Historically, patterns observed in consumer vehicle sales provide a backdrop for understanding the current situation. The automotive industry's response to economic downturns often reveals resilience but also exposes vulnerabilities. For example, after the 2008 financial crisis, vehicle sales dropped significantly, resulting in manufacturers revising strategies for economic uncertainty. Fast-forward to 2020, when the COVID-19 pandemic wreaked havoc on global supply chains, pushing vehicle sales to unprecedented lows.

The subsequent recovery patterns post-COVID highlighted a complex interplay between consumer confidence, supply chain stability, and government mandates. It’s a reminder of how interconnected these elements are. December's performance, when viewed through this lens, necessitates cautious optimism rather than outright celebration.

Implications for the Future

So, what does this mean for the automotive industry going forward? The initial uptick may give a sense of recovery, but the broader economic outlook remains uncertain. Rising interest rates and inflation could dampen consumer spending, and if economic pressures mount, sales figures could significantly decline in the months ahead. Knowing these challenges, manufacturers would do well to closely monitor economic indicators and adjust production and marketing strategies proactively.

Retail prices also remain a contentious issue. As automakers strive to maintain margins in the face of escalating production and material costs, consumers might find themselves facing higher prices. This creates a paradox where even with rising sales numbers, the vitality of the market may diminish if affordability becomes an obstacle.

And yet, there's potential for innovation. Manufacturers investing in advancements like hybrid technologies and EVs could not only appease current buyers but help prepare for a more sustainable future that regulators and consumers increasingly demand.

Conclusion: A Watchful Eye Required

With December’s sales data in hand showing a mixed picture of short-term growth amid long-term challenges, the months ahead will demand a watchful eye. The automotive industry, characterized by cyclical trends, must navigate these uncertain waters with strategic precision. The ups and downs we’re seeing now could signify larger market trends influenced by broader economic realities.

The numbers reflect complexities that go beyond mere totals and percentage changes. They hint at a marketplace grappling with change yet poised for potential transformation. As we continue to analyze the trends, one thing remains clear: adaptability will be the name of the game for the automakers willing to thrive in these challenging yet opportunity-ridden times.

Click on graph for larger image.

Click on graph for larger image. The second graph illustrates light vehicle sales from 1967 onwards. In a slightly positive twist, December's numbers exceeded analyst expectations, contributing to an overall growth of 2.4% in vehicle sales for 2025 relative to 2024.

The second graph illustrates light vehicle sales from 1967 onwards. In a slightly positive twist, December's numbers exceeded analyst expectations, contributing to an overall growth of 2.4% in vehicle sales for 2025 relative to 2024.